Record market gains, record revenues, record poverty. Nigeria’s economy is growing, but too many Nigerians are not.

The trading floor is celebrating.

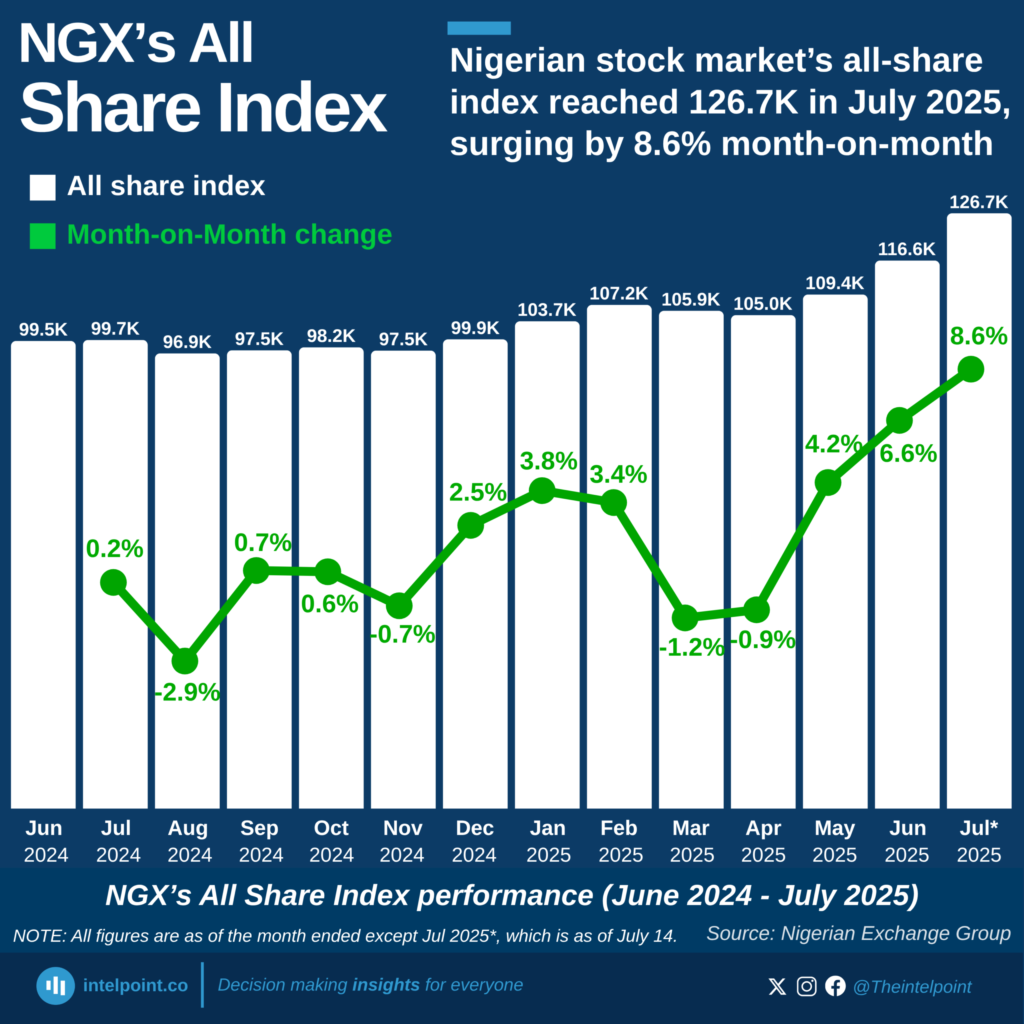

The Nigerian Exchange has become one of Africa’s strongest-performing stock markets. The All-Share Index has surged to historic highs. Market capitalisation has crossed ₦160 trillion. Banking stocks have soared. Telecommunications companies are reporting robust earnings. Investors are applauding reforms. International rating agencies are upgrading outlooks. Government officials point to rising revenues and renewed investor confidence as proof that the economy is turning a corner.

Yet outside the trading floor, a different Nigeria exists.

Food remains expensive.

Transport remains expensive.

Housing remains expensive.

Electricity remains unreliable.

Jobs remain scarce.

And according to recent estimates by the World Bank, more than 140 million Nigerians live in poverty.

These realities are not contradictory.

They are connected.

Indeed, they reveal one of the defining features of Nigeria’s economic moment: the growing disconnect between financial prosperity and social wellbeing.

The stock market is booming.

The people are still waiting.

The Market Is Not the Economy

One of the most common mistakes in economic discourse is assuming that a rising stock market automatically means a prosperous society.

It does not.

The Nigerian Exchange measures the performance of listed companies, not the welfare of citizens.

A stock market can rise because banks are profitable, telecommunications firms are expanding revenues, and institutional investors are purchasing shares. None of this necessarily translates into improved living conditions for the average Nigerian.

Nigeria’s economy is overwhelmingly informal. Millions of citizens earn their living through petty trading, small-scale farming, transportation, artisanal production, and informal services. Most of these activities are not represented on the exchange.

When the stock market rises, it reflects the fortunes of corporate Nigeria.

It does not automatically reflect the fortunes of market women in Ado-Ekiti, commercial drivers in Kano, traders in Onitsha, or fishermen in Bayelsa.

The distinction matters because policy makers increasingly point to market performance as evidence of national progress.

But a rising index is not a substitute for rising living standards.

The Inflation Effect

Part of the recent stock market surge is undoubtedly a reflection of improved investor confidence.

Part of it is also inflation.

Nigeria has experienced one of the most significant inflationary periods in its modern history. The removal of fuel subsidies, exchange-rate liberalisation, rising energy costs, and supply-chain disruptions have pushed prices sharply upward.

In such an environment, nominal asset values tend to rise.

Corporate revenues increase because prices increase.

Asset values increase because money loses purchasing power.

Equity prices increase because investors seek protection against inflation.

This creates the appearance of extraordinary growth.

But appearances can be deceptive.

A company whose revenues have doubled while costs and prices have doubled may not be creating substantially more economic value.

Likewise, an investor earning a 40 percent return in a high-inflation environment may not be substantially wealthier in real terms.

For households without financial assets, however, inflation is not an accounting exercise.

It is a daily struggle.

The same forces driving market gains are often driving hardship.

Who Benefits?

Perhaps the most important question is not whether the market is growing.

It is who owns the growth.

Stock market participation in Nigeria remains limited.

The overwhelming majority of citizens do not own equities directly. Many have no brokerage accounts, no investment portfolios, and little exposure to capital markets.

The beneficiaries of market rallies are therefore concentrated among:

- Institutional investors

- Pension fund administrators

- High-net-worth individuals

- Corporate executives

- Foreign portfolio investors

This concentration of ownership means that gains in financial markets often remain confined to a relatively narrow segment of society.

Meanwhile, workers, farmers, artisans, and small business owners experience little or no direct benefit.

The result is an economy where wealth creation and wealth distribution increasingly move in different directions.

The Currency Challenge

The naira’s depreciation has further complicated the picture.

While exchange-rate reforms may have improved transparency and corrected longstanding distortions, they have also imposed significant costs on households.

Imported goods have become more expensive.

Manufacturing inputs cost more.

Transportation costs have risen.

Food inflation remains stubbornly high.

For investors, equities can serve as a hedge against currency weakness.

For ordinary Nigerians, there is no such protection.

They absorb the cost directly.

This is why market gains can coexist with declining purchasing power.

The people who own financial assets are often shielded.

The people who depend solely on wages and small business income are not.

The Missing Link

Economic growth becomes meaningful only when it improves people’s lives.

That requires a transmission mechanism.

In successful economies, corporate profitability leads to investment.

Investment leads to production.

Production creates jobs.

Jobs generate income.

Income improves living standards.

Nigeria’s challenge is that this chain remains weak.

Many companies are generating higher profits without corresponding increases in employment.

Others are achieving stronger earnings through pricing power, exchange-rate adjustments, and financial restructuring rather than expanded production.

The result is a market that rewards capital more effectively than labour.

A society where shareholders advance while workers struggle cannot sustain social stability indefinitely.

The Real Measure of Success

The true measure of economic success is not market capitalisation.

It is human wellbeing.

Can families afford food?

Can young people find jobs?

Can small businesses survive?

Can parents educate their children?

Can workers maintain a decent standard of living?

These are the questions that matter.

A rising stock market is welcome.

Strong corporate performance is desirable.

Investor confidence is important.

But none of these should be confused with broad-based prosperity.

The purpose of an economy is not merely to generate wealth.

It is to improve lives.

What Must Change

Nigeria does not need to choose between a strong stock market and a prosperous society.

It should have both.

But achieving that outcome requires deliberate policy choices.

Government must deepen financial inclusion so more Nigerians can participate in wealth creation.

Pension coverage must expand beyond the formal sector.

Small and medium-sized enterprises must gain greater access to affordable credit.

Manufacturing and agriculture must receive sustained support to generate productive employment.

Most importantly, economic policy must be evaluated not only by what it does for markets, but by what it does for people.

A Final Word

The Nigerian Exchange is telling one story.

The streets are telling another.

The market says confidence is returning.

The people say hardship remains.

Both stories are true.

The challenge before policymakers is to ensure they eventually become the same story.

Because a booming stock market in a country struggling with widespread poverty is not evidence that prosperity has arrived.

It is evidence that prosperity remains unevenly distributed.

Until growth reaches households with the same force that it reaches balance sheets, Nigeria’s economic recovery will remain incomplete.

And every new market record will continue to provoke the same uncomfortable question:

If the economy is doing so well, why do so many Nigerians still feel left behind?